Finance

» Renewable Energy Projects

The Optimum Financing Structure

With so many different financing structures to choose from, which one is the optimum? That very much depends on the project itself as well as the participants. As with other infrastructure projects, capital intensive energy projects are often financed as stand-alone entities (Project Finance) rather than as part of a corporate balance sheet (Corporate Finance). The main advantages of project finance are:

- Non-recourse/limited recourse financing: There is no or only limited recourse to the project sponsor's assets for the liabilities of the project. Thus, the project preserves the sponsor's debt capacity.. Also, lenders will be more keen to participate in a workout.

- Risk Sharing: By setting up a separate legal entity, the project risk is isloated and can be allocated to the parties that can best control, understand and mitigate the risks involved. Consequently, incentives for all involved are optimized. This includes political or country risk.

- Favourable Tax Treatment: Project Finance structures allow tax benefits to be allocated to entities that can make use of them.

- Improved Financing Terms: The project may obtain more favourable finnacing term than it would based on the sponsor's credit profile alone. This way projects can be carried out that would be too big for one sponsor.

However, all of these benefits come at a high transaction cost, higher interest rates and insurance coverage. |

How to choose the Financing Structure?

The developer who initiates the project decides which finnancing structure best meets their needs for a project based on multiple considerations.

|

| Consideration / Motivation |

Context |

Most suitable structure |

| Project Size |

If the project's value is less than $50m, the transaction costs of Project Finance will outweigh the benefits. |

Corporate |

| Developer can use tax benefits |

If the developer wants to use tax benefits, the project needs to be on its balance sheet. However, often, developers are much smaller than the projects they develop and have no capacity to use all the tax benefits. |

Corporate |

| Developer can fund project costs |

If the developer can fund project costs |

Corporate

PAYGO |

| Low Project IRR |

If the project's projected internal rate of return (IRR) is low, increasing debt levels will help increase the equity holder's rate of return. |

Leveraged Structure |

| Developer wants early cash distribution |

Due to the large capital expenditure there are no early cash distributions available if developed on own balance sheet. The developer either needs to sell early, or device a structure wehereby the developer receives a large proportion of cash. |

Project Sale

Back-leveraged PAYGO |

| Re-financing |

If the projeect already exists, but just needs re-financing, possibly after construction, options include a pay-as-you-go structure or leasing. |

PAYGO

Leveraged Lease |

|

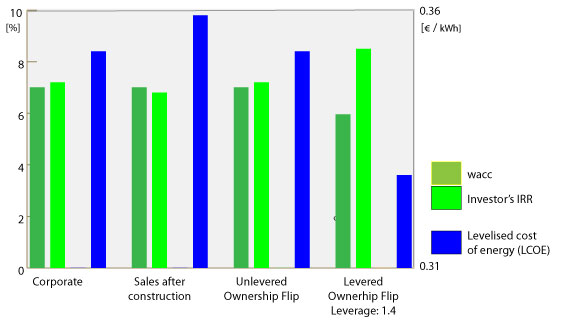

Impact of financing structure on returns and the cost of energy

The investor's internal return and the plant's levelised cost of energy vary with the choice of financial structure. The investor's internal return and the plant's levelised cost of energy vary with the choice of financial structure.

We have calculated the weighted average cost of capital, investor's internal rate of return and the levelised cost of energy for investment in a 1MW solar park for different financing structures.

The levered structure yields the highest return and lowest cost of ownership because of the lower cost of debt and the tax shield provided by the debt. Also, the debt lowers the average cost of capital, though increases the expected return for the investor.

The cost of ownership is highest in the "sales after construction" scenario, as the interest for financing the construction before the sale has been added to the capital cost of the whole plant. |

Join us

|

Join us on Linkedin

Subscribe to our blog

Follow us on Twitter

Follow us on Facebook

|

<< previous | next >> |

|